This article by Chris Ragan, Paul Rochon, and Mark Jaccard originally appeared in The Hub. A similar op-ed appeared in The Globe and Mail on June 4, 2023.

The federal government has embraced the objective of reducing Canada’s greenhouse-gas emissions to “net zero” by 2050, and many policies are being introduced to move the country in this direction. Given the large fraction of Canada’s emissions that come from the oil and gas sector, it is not surprising that many people argue the need to “phase out” this production as a central plank of our emissions-reduction strategy.

In response to such arguments, one might ask whether there is a lower-cost way to reduce Canada’s GHG emissions. What would be the economic cost to the country of intentionally shrinking our oil and gas production, and is it necessary to bear this cost? These are crucial questions for thinking about the future of Canadian climate policy. The purpose of this essay is to review a recent report from the Public Policy Forum which examines the economic cost of phasing out oil and gas production, and compares it to an alternative policy approach, both of which can achieve the net zero target by 2050. The bottom line is straightforward: an intentional phase-out of oil and gas production is not necessary for Canada to achieve its net zero target, and the costs of using such a policy approach would likely be enormous. To reduce the overall cost of achieving the 2050 target, the government should be encouraged to pursue policies that apply more-or-less equally to all sectors and regions of the country.

Section 1: More Climate Policies Needed

The Canadian government has made a clear commitment to achieve net zero greenhouse-gas (GHG) emissions by 2050. Canada is not alone; many advanced countries are committed to making the same transition. Given the energy intensity of advanced economies, and the carbon intensity of their energy systems, the emissions-reduction policies we employ will have enormous economic implications. We can expect disruption costs associated with moving away from high-emitting systems, development costs associated with the creation of low-emitting systems, and many economic opportunities associated with the development and sales of new and cleaner technologies.

With Canada facing many economic challenges, from population aging and low productivity growth to strained health-care systems and rising protectionist forces among our trading partners, our climate policies should be designed to achieve their objectives at the lowest possible cost. Higher-then-necessary costs imply that we are forgoing resources that could be used to finance many important social and economic objectives. Would it be sensible to pursue high-cost policies if the same environmental benefits could be achieved at significantly lower cost?

Mindful of the appeal of reducing costs, governments in Canada have implemented economy-wide carbon prices, a policy approach widely recognized as the most flexible and lowest-cost option. Some provinces have designed and implemented their own carbon-pricing systems; the federal carbon-pricing “backstop” applies in those jurisdictions which have chosen not to do so. As a result, carbon pricing now exists in all regions of Canada, and according to the OECD applies to over 82 percent of our total GHG emissions.

The federal government is rightly proud of Canada’s policy approach, as is clear from this statement in the 2023 federal budget:

“Canada has taken a market-driven approach to emissions reduction. Our world-leading carbon pollution pricing system not only puts money back in the pockets of Canadians, but is also efficient and highly effective because it provides a clear economic signal to businesses and allows them the flexibility to find the most cost-effective way to lower their emissions. At the same time, it also increases demand for the development and adoption of clean technologies.” (page 71)

Canadian governments have also implemented a range of other climate policies, aimed at reducing GHG emissions without the use of carbon prices. These complementary policies have been pursued partly because carbon pricing may not be practical in all situations and partly because relying purely on rising carbon prices to reduce emissions may be viewed as politically unacceptable. The upshot is that Canada now employs a complex collection of climate policies: provincial and federal policies, some based on carbon taxes, others based on cap-and-trade systems, and still others based on regulations, subsidies, and tax credits.

Yet the current package of climate policies is insufficient to get Canada to its net zero objective by 2050, and there is still considerable debate as to whether current policies are stringent enough to accomplish our more modest 2030 targets. The implication for Canada’s climate policies, at least for achieving the 2050 objective, is clear: we will need to add more policies to the package or increase the stringency of existing policies. What is the best policy path forward?

Since Canada’s oil and gas sector is the source of a significant fraction of our total GHG emissions, approximately 28 percent in 2021, it is not surprising to hear many Canadians, including some environmental groups, think tanks, and political parties, arguing in favour of “phasing out” oil and gas production. For example, in a 2018 report published by two prominent environmental groups, we are told that “Canada appears intent on finally addressing climate change and building a low carbon economy, but the idea that this can be done without extensive cuts in oil and gas production is a fallacy.” The report goes on to advocate the implementation of “policies that restrict the supply of oil and gas from Canada.”

In 2022, the federal government proposed an “emissions cap” for Canada’s oil and gas sector. No details have yet been released on how this cap will be implemented, and such details matter greatly, especially if we want to ensure that our overall climate policies are cost-effective. Though the federal proposal for an emissions cap is not equivalent to a phase-out of oil and gas production, the narrative around the need for a sector-specific emission cap sounds much like the narratives that argue for production phase outs.

These arguments often fail to make the crucial distinction between GHG emissions, which are rightly the target of climate policies, and fossil-fuel production itself, which is conceptually distinct from the associated emissions.

Three comments should be made about this distinction. First, humanity has long had technologies to convert fossil fuels into zero-emission hydrogen or electricity while capturing and sequestering carbon to prevent GHG emissions, and these technologies might expand dramatically as more countries adopt aggressive climate policies. While this chemical transformation could occur in an oil-producing country like Canada, which then might export electricity or hydrogen, it could also occur in countries that import our oil. Second, Canada and the countries importing our oil might continue burning some refined petroleum products (like jet fuel) provided that all resulting GHG emissions are offset by some form of direct air capture. This is the essence of targets like “net-zero” as opposed to just “zero.” Third, some oil serves as a material feedstock in the production of lubricants, plastics, asphalt, tar, bulk chemicals, fertilizers and other non-energy products, which do not lead to GHG emissions because the oil is not combusted. For these reasons, the reduction of GHGs and the phase-out of oil production should be seen as distinctly different objectives with potentially large differences in costs.

The recently released report which is the subject of this essay is based on an economic-environment modelling exercise conducted by Navius Research Inc., a consulting firm that has done energy-economy-emissions research for most provincial and territorial governments, the federal government, and a range of NGOs, including the Canadian Climate Institute and Canada’s Ecofiscal Commission.

The PPF/Navius report compares two policy approaches for Canada to achieve net zero GHG emissions by 2050. The first approach is “aggressive decarbonization”: it includes Canada’s current package of climate policies and adds a country-wide carbon price which rises sufficiently to achieve net zero emissions by 2050. The second approach is an “oil and gas production phase-out”: it begins with Canada’s current policy package, adds a phase-out of oil and gas production beginning in 2035, and then completes the policy package with a country-wide carbon price that rises as necessary to achieve the net zero objective.

Given these alternative policy approaches—which both achieve net zero by 2050 but differ in terms of the policies employed—the central goal is to compare the economic aspects of the outcomes. Does one of these approaches cost more than the other in terms of national income and, if so, how much is that extra cost? If the cost difference between the two approaches were negligible, one could argue that the choice between the two approaches is of little economic importance. But if the cost difference were significant, then Canada’s policymakers would have a solid reason to favour the less costly approach.

To anticipate what follows, the PPF/Navius report shows that the costs of the two policy approaches are quite different—a significant economic cost would accompany a phasing out of oil and gas production. It would be significantly less costly for Canada overall, and massively less costly for Alberta, to achieve our net zero objective by relying on a collection of policies applying to all sectors and regions more-or-less equally, such as an economy-wide carbon price. This is the reasoning behind the word “excessive” in this essay’s title. The economic cost associated with phasing out Canada’s oil and gas production would be excessive because it would be unnecessary—since less costly policy approaches exist to achieve the same emissions objective.

Section 2: Comparing Two Policy Approaches

Given the objective of achieving net zero GHG emissions by 2050, the central question addressed in this essay is:

What is the economic impact of achieving this objective by requiring a reduction in Canadian oil and gas production below the level that would naturally occur as that sector responds to the future evolution of the global and domestic market during a period of intensifying human action to address climate change?

The idea that Canada’s oil and gas sector will naturally respond to the “future evolution” of markets is central. The evolution of these markets includes factors such as the global prices of oil and gas, climate policies in other countries, the technology and prices of electric vehicles and batteries, the development and costs of carbon capture and storage, improvements in wind and solar technologies, better and cheaper storage of electricity, and many other things. As these various elements change over time, the global demand for fossil fuels will change, and so too will the demand for Canadian oil and gas. Under some possible future scenarios, Canadian production will decline sharply between now and 2050; in others it will decline but only gradually; in still others, considerable demand for Canada’s oil and gas will persist for many years. There are many forecasts of how the global market might evolve, perhaps the most prominent being the World Energy Outlook from the International Energy Agency. But the truth is that we simply cannot know how the future will unfold.

Given the extent of this uncertainty, how do we answer our central question? For the key variables such as those mentioned above, we imagine many possible values within a realistic range. Any one combination of these values across the several variables defines a single scenario.

For each scenario, we compare the implications of the two alternative policy approaches, emphasising the outcomes in 2050. We then repeat this exercise, scenario by scenario, so we can compare the two policy approaches across many possible scenarios. None of this is simple.

The PPF/Navius report provides a coherent way to approach our question by employing a detailed mathematical model of the Canadian economy and GHG emissions and using this model to compare the “aggressive decarbonization” and “production phase-out” policy packages. Each policy package is constructed to ensure that net zero GHG emissions is achieved in Canada by 2050, and so they are environmentally equivalent. The focus can then be on the key economic differences between the two policy approaches.

Some key elements and assumptions used in the Navius model are worth explaining.

General Equilibrium Model

The Navius model, which is specifically designed for comparing the economic impacts of different climate and energy policies, is what economists call a “general equilibrium” model, meaning that all markets and sectors are assumed to simultaneously attain a supply-and-demand equilibrium through adjustment of the relevant market price. This is a much-debated modelling approach for assessing many short-run macroeconomic issues, such as the causes of recessions and the duration of high unemployment. But our central question is one which applies mostly to a long-run perspective, as we are comparing the economic implications of two policy approaches over a period of almost 30 years, and for these kinds of long-run questions, the use of such a model is appropriate.

World Oil Prices

The Navius model considers a range of world oil prices—a key variable influencing how much oil is produced in Canada during any year. There is obviously significant uncertainty regarding the future world oil price. It is possible, for example, that Canada and other countries will continue to use a considerable amount of oil but rely heavily on widely available and low-cost carbon capture and storage (CCS) or direct air capture (DAC) to prevent or offset any associated GHG emissions. In such a world, the demand for oil would likely remain strong, preventing the world oil price from falling. Alternatively, these two technologies may prove to be too ineffective or too expensive and, at the same time, the costs of other low-emitting energy systems, like renewables or nuclear, could fall considerably because of technological breakthroughs. These conditions would combine to make it much less attractive for the continued use of oil in any country, and this would lead to less global demand and a low world oil price.

Different future pathways for technological developments thus have different implications for future oil demand, and therefore for the future world price of oil. Considering this uncertainty, it is important to account for different possible futures using sensitivity analysis, rather than to make specific assumptions about the future price. In the PPF/Navius report, three different paths for world oil prices to 2050—low, intermediate, and high—are considered, based on forecasts made by the Canadian Energy Regulator, which are broadly comparable to separate forecasts made by the International Energy Agency and the U.S. Energy Information Administration. Over the 25-year modelling period, the assumed world oil price (in U.S. dollars per barrel of WTI) ranges between $35 and $95, with an average price of about $65.

The Cost and Availability of Direct Air Capture (DAC)

Direct air capture is not yet a widely available technology and there remains considerable uncertainty about whether it will become commercial and, if so, at what cost. It is an important technology to consider in this analysis, however, because its availability and cost have significant implications for how Canada can achieve net zero. The potential availability of large-scale and low-cost emissions reductions using DAC could provide significant flexibility and reduce the overall economic cost of achieving net zero by allowing for the continued production and combustion of fossil fuel products. In the PPF/Navius report, four different scenarios for the availability and cost of DAC technology are considered: unavailable, low cost, intermediate cost, and high cost, the last three based on the minimum, average, and maximum projected costs reported in the specialized literature on this topic.

The Cost of Carbon Capture and Storage (CCS)

In some industrial activities, capturing and storing carbon emissions is one of the few cost-effective ways to significantly reduce emissions without dramatically reducing the output of the product itself. For example, opportunities to reduce emissions from process heat or cogeneration in the oil and gas sector are limited. As a result, future cost declines for CCS technologies can have significant implications for the ability of this sector to achieve significant emissions reductions, making uncertainty in these future costs an important dynamic to examine in this analysis. As noted above, CCS can be associated with the production of combustible fossil fuel products (like gasoline and diesel), but can also be associated with the conversion of any fossil fuel to hydrogen or electricity while preventing the CO2 byproduct from reaching the atmosphere. In the PPF/Navius report, three different scenarios for the cost of CCS technology are considered—low, intermediate, and high—based on studies from the Global CCS Institute and the International Energy Agency.

Section 3: The Main Results

As is clear from the PPF/Navius report as well as recent work by the Canadian Climate Institute, there are many pathways Canada can take to get to net zero emissions by 2050. Canada can achieve net zero whether world oil prices are high or low, whether direct air capture is available or not, whether carbon capture and storage is economical or costly, and whether we rely primarily on aggressive carbon pricing or choose instead a collection of very different policies. None of this means that getting to net zero will be easy; it will require the implementation of stringent policies, an enormous amount of investment in cleaner technologies, and Canadian consumers and businesses to make many changes to current consumption patterns and production methods. Put differently, Canada has many options regarding which policies it chooses to get to net zero.

Recall that the PPF/Navius report models two alternative policy packages to achieve net zero by 2050. The first is the “aggressive decarbonization” policy package. It is based on Canada’s current policies plus a country-wide carbon price which rises as necessary to achieve the net zero target. The second alternative is the “production phase-out” package. It also is based on Canada’s current policies but adds a phase-out of Canadian oil and gas production beginning in 2035. This package is completed with a country-wide carbon price which rises as required to achieve the net zero target.

We now examine three central results from the PPF/Navius report, emphasizing the path of carbon prices, the impact on Canadian GDP, and the impact on Alberta’s GDP.

The Path of Carbon Prices in the Two Policy Approaches

The aggressive decarbonization policy approach relies largely on a rising economy-wide carbon price to achieve the net zero objective. The federal government’s “backstop” carbon price is currently scheduled to rise to $170 per tonne by 2030. In the report’s modelling exercise, using the “intermediate” scenario, the economy-wide carbon price continues rising for the twenty years beyond 2030, reaching about $500 per tonne by 2050.¹ To put this in perspective, a $500 per tonne carbon price translates into total carbon-related fuel charges for gasoline of about $1.10 per litre, which would result in Canadian gasoline prices by 2050 roughly equivalent to those in France today. For those who worry about the impact of such gasoline prices, it is worth noting that the modelling shows only a tiny percentage of Canadian drivers still burning gasoline by 2050 since by then zero-emission vehicles will likely be far cheaper to own and operate.

If Canada instead chooses the oil and gas production phase-out approach, a large amount of emissions reductions are occurring in the oil and gas sector. As a result, the carbon price which applies to the non-oil-producing part of the economy needs to drive fewer emissions reductions and thus does not need to rise as much. In the same intermediate scenario, the model generates a carbon price that reaches $450 per tonne by 2050.

A comprehensive measure of the economic costs associated with each scenario is found by examining the differential impacts of the two policy approaches on national income, most often measured using Gross Domestic Product (GDP). We turn to this now.

Canada’s GDP in the Two Policy Approaches

Table 1 below shows the average annual growth rate of real GDP for Canada from 2020 through 2050, under the two policy approaches, assuming the intermediate scenario but also allowing for three different world oil prices. Note that Direct Air Capture (DAC) technology is assumed to be unavailable in these scenarios. For both scenarios, the growth rates shown are far more precise than any conventional economic forecast would ever display, but the point here is not to take the precise growth rates literally but to focus instead on the approximate difference in the growth rates across the two policy approaches.

For each of the three world oil prices, these results suggest a clear cost in real GDP associated with using the oil and gas production phase-out rather than the policy approach which places primary emphasis on a uniform, economy-wide carbon price. Notice that the reduction in the average GDP growth rate associated with the production phase-out becomes larger when the world oil price is higher; in the low oil price scenario, the cost is only 0.03 percent annually, whereas in the high oil price scenario the cost is 0.22 percent annually. The logic of this result is straightforward: when the world oil price is higher, the national income generated by oil and gas production is naturally higher, and thus the GDP sacrifice associated with not producing this oil and gas becomes commensurately larger.

These differences in annual GDP growth rates appear small, but after many years they accumulate into large differences in the economy’s overall GDP. For example, using the high oil price scenario, the difference in real GDP by 2050 is about $200 billion, roughly 7 percent of GDP at that time. This is the GDP cost of using the production phase-out approach as opposed to the aggressive decarbonization approach. This GDP reduction is equivalent to twice the size of the recession Canada experienced during the 2008 Global Financial Crisis—but unlike that recession which lasted a little more than a year, the GDP cost in Table 1 is permanent. By contrast, in the low world oil price scenario, the 2050 GDP difference is about $27 billion, just under 1 percent of GDP at that time. In this scenario, the production phase-out of oil and gas still imposes a cost on the economy, but since that production is less valuable on world markets, the cost of sacrificing that output is also lower.

These findings underline three important points. First, under most imaginable scenarios, phasing out the production of oil and gas would impose a cost on the Canadian economy—for the simple reason that we would be sacrificing economic production that would otherwise generate national income. Second, the size of that cost depends importantly on the global context, and especially on the world oil price. The higher is the world oil price, the more costly it would be to phase out the production of oil and gas. Third, the cost of the production phase-out is “excessive” in the sense that it is unnecessary; a lower-cost policy approach is available to achieve the same emissions objective.

One final comment about the results in Table 1. These scenarios embody the assumption that Direct Air Capture (DAC) technology is unavailable, and also that the cost of Carbon Capture and Storage (CCS) is at its intermediate level. But if DAC technology becomes available during the next three decades, or the costs of CCS technology fall significantly, the attractiveness of fossil fuels will be enhanced. The result will be a greater likelihood of the high world oil price scenario. In other words, while most imaginable scenarios indicate a clear and significant GDP cost associated with a phase-out of Canadian oil and gas production, this cost would be even higher if CCS and DAC become more available and more cost-effective.

What about employment and wages with the two policy approaches? Given the negative impact on real GDP from imposing a production phase-out, one might think that Canadian employment would also be significantly and adversely affected. But the “general equilibrium” model employed in the PPF/Navius report is one in which all markets, including labour markets, are brought into equilibrium through adjustments in the relevant market prices—in this case, real wages. As mentioned above, this “full employment” assumption is problematic when the issues being examined are short-run business cycle fluctuations, but for long-run analyses including technological change and economic growth, this assumption is much more realistic.

With the assumption that real wages adjust to keep labour markets in a state of equilibrium, we can gain a better understanding of how the overall economy would likely adjust if Canadian policy imposed a phase-out of oil and gas production. This phase-out would naturally lead to a decline of employment in that sector. Those displaced workers would eventually get re-absorbed into other sectors but only as a result of a decline in their real wages. The total level of employment in the economy would be largely unaffected, as it is driven mostly by changes in workers’ preferences and labour supply. But the labour force would be reallocated across sectors, away from the oil and gas sector and toward many other sectors which expand as a result. Note, however, that workers would be leaving a sector with very high labour productivity (oil and gas production) and be reabsorbed into sectors which, on average, have much lower labour productivity. Thus, while overall employment in the economy would not be largely affected, total income accruing to workers and overall national income (GDP) would fall, and possibly very significantly—as the numbers in Table 1 clearly suggest.²

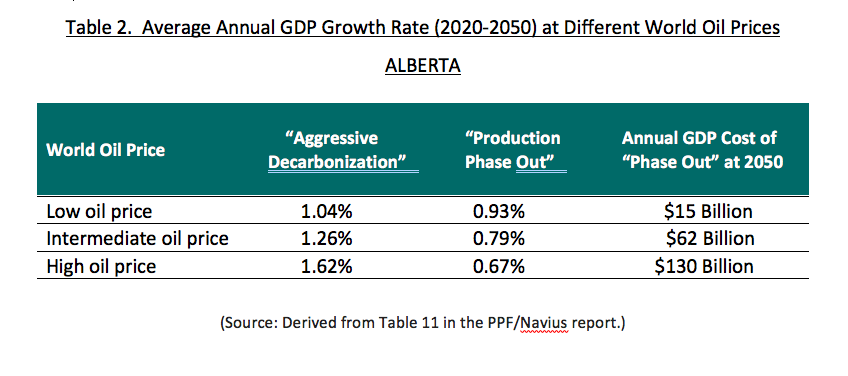

Alberta’s GDP in the Two Policy Approaches

We have discussed the cost to Canadian GDP that would likely arise from using a phase-out of oil and gas production as part of an overall climate policy package. Since most Canadian oil and gas is produced in Alberta, it should not be surprising to learn that the economic impact of this policy approach would be concentrated in that province. But how big an impact would it be?

Table 2 below shows the same analysis as Table 1, but specifically for Alberta. The average GDP growth rate for 2020-2050 is shown for the two alternative policy approaches, assuming the intermediate scenario and three different world oil prices.

To begin, note that in the aggressive decarbonization policy package, the Alberta economy displays average GDP growth rates above 1 percent annually even if the world oil price is low, and a considerably higher growth rate (coming partly from increased oil and gas production) when the world oil price is high.

If Canada instead employed a production phase-out approach, the impact on Alberta’s GDP growth would be significantly negative; the annual growth rate would be reduced by about 0.1 percent when world oil prices are low and by almost 1.0 percent when the world oil price is high.³ These changes in annual growth rates result in large differences in the level of real GDP in 2050. In the case of the intermediate world oil price, the GDP cost to Alberta of the production phase-out approach is about $60 billion, approximately 15 percent of Alberta’s GDP at that time. At a high world oil price, the GDP cost would be $130 billion—over 30 percent of provincial GDP.

The GDP costs shown in Table 2 are enormous. The Canadian recession caused by the COVID-19 pandemic was the deepest the country has experienced since the Great Depression in the 1930s, with real GDP falling by about 15 percent. As bad as that was, the sharp economic decline persisted for less than half a year during the middle of 2020, and three years later the economy was close to fully recovered. In contrast, the GDP costs shown in Table 2 would be just as large (and perhaps larger) for Alberta’s economy as the COVID recession was for Canada’s, but in this case the costs would be permanent and ongoing. Put differently, the PPF/Navius modelling exercise suggests that the imposition of an oil-and-gas production phase-out would be akin to permanently eliminating one in every 5 or 6 dollars generated in Alberta’s 2050 economy.⁴

Some additional costs not shown in the Navius model would be especially important in Alberta: the short-term transitional costs incurred because of the policy-driven phase-out of oil and gas. For example, as oil-patch workers would be laid off due to production cuts, there would be considerable costs as they experience unemployment, search for new jobs, change their locations, invest in retraining, and eventually get re-employed in a different economic sector, possibly even in another Canadian province. The same would apply to many businesses involved in servicing the oil and gas sector. The production cuts would lead to less demand for their services, and there would be real costs involved as these businesses redirect their capital, entrepreneurial efforts, and labour forces to more productive and profitable activities. In the Navius model, these costs are absent because the model assumes full employment; but in the real world such costs are very relevant and often quite considerable, even if they last for only a few years.

Section 4: Taking the Model Seriously But Not Literally

Economic models should never be taken as literal representations of the economy, but they should be taken seriously if they produce useful insights about how various parts of the economy fit together. The Navius model is not designed to provide precise forecasts of the future, but rather to examine the approximate impacts of different kinds of climate policies. It is especially useful for emphasizing the differences between alternative policy approaches, which is the central objective the PPF/Navius report.

The two alternative policy packages examined in that report should also not be taken as exact or literal descriptions of specific policies. The “aggressive decarbonization” policy approach appears in the model as an economy-wide carbon price which rises as necessary to achieve the net zero target by 2050. But its broad economic impact would be very similar to any collection of economy-wide policies which resulted in approximately equal marginal abatement costs across regions and sectors. These might include, for example, “flexible” regulations that incorporate compliance trading among large GHG emitters, such as British Columbia’s Low Carbon Fuel Standard or the Clean Fuel Regulations currently being developed by the federal government.

The “production phase-out” policy approach appears in the model as a gradual, forced reduction in oil and gas production beginning in 2035. This would be a reasonably accurate depiction of any policy-driven output reduction of this magnitude that occurs over this time frame.

Taking the modelling results in the PPF/Navius report seriously but not literally, we can summarize the key findings:

- Broad-based and economy-wide policies can be used to achieve net zero GHG emissions by 2050. A policy which phases out Canadian oil and gas production is not necessary to achieve this objective.

- Employing an active phase-out of Canadian oil and gas production would increase the economic cost of achieving net zero, possibly by as much as several percentage points of GDP by 2050.

- The GDP cost associated with a policy-driven phase-out of oil and gas would depend importantly on market conditions, including the costs of DAC and CCS and the world price of oil. The higher is the price of oil, and the lower are the costs of DAC and CCS, the larger would be the economic cost of phasing out oil and gas production.

- The economic cost of phasing out Canadian oil and gas production would be especially large for Alberta. Under some reasonably likely market conditions, the cost to Alberta could be well over 15 percent of GDP by 2050, and maybe as much as 30 percent.

Section 5: Final Remarks

Two characteristics of GHG emissions are central to the choice of effective and low-cost climate policies. First, GHGs are emitted from hundreds of thousands of point sources, from cars and trucks, to homes and buildings, to manufacturing processes and electricity-generating stations. And the costs of reducing GHG emissions vary widely across these many regions, sectors, and facilities. Second, every tonne of GHGs emitted enters the same atmosphere and creates the same problems with respect to the global climate. The climate makes no distinction between a tonne of emissions from Edmonton and a tonne of emissions from Etobicoke.

Given these two characteristics, an economy-wide carbon price is widely recognized to be the lowest-cost approach for reducing emissions. A well-designed carbon price applies to all emitters, regardless of size or sector, who are then incentivised to find the lowest-cost way to avoid emitting GHGs. The resulting emissions reductions are typically not spread equally across regions or sectors but instead are allocated in such a way that minimizes the overall abatement costs, thereby being most supportive of economic growth.

In contrast, climate policies that are focussed on specific regions or sectors face the real risk of reducing GHG emissions at much higher overall costs; “excessive” costs in the sense that lower-cost policy options are available to accomplish the same level of emissions reductions.

This central logic of using carbon pricing to achieve low-cost emissions abatement is the basis of current Canadian climate policy, especially at the federal level. The current federal “backstop” carbon price is scheduled to rise to $170 per tonne by 2030. But as we consider adding either more policies or more stringent policies to the overall policy package to achieve our 2030 targets, as well as our more ambitious net zero objective for 2050, Canadian policymakers should be mindful of the importance of using low-cost policies whenever possible.

Many Canadians seem to think that phasing out the production of Canadian oil and gas would be an effective way for the country to achieve its net zero objective. And there is no doubt that using such a policy approach could very significantly reduce GHG emissions. The problem is that the economic costs of taking such an approach would be very high. This essay has reviewed a recent PPF/Navius report which shows that, depending on the world oil price over the next 30 years, the cost of using a production phase-out approach would likely be between 1 and 7 percentage points of Canadian GDP by 2050, and this would be a permanent, ongoing cost. Since the phase-out of oil and gas would apply most critically to Alberta, the impact on that province’s GDP would be considerably higher, and perhaps even as high as 30 percent of provincial GDP.

Nobody should be surprised to learn that actively phasing out oil and gas production in Alberta—more actively than might occur as that sector responds to evolving global climate policies and market forces—would impose a large economic cost on that province. What is more, it would surely exacerbate existing political and regional tensions in Canada and provide many Albertans with tangible and immediate arguments against an over-stepping federal government.

If phasing out the production of Canada’s oil and gas were essential for reducing our GHG emissions, it would be a more understandable approach. But what the PPF/Navius report highlights so clearly is that an intentional and policy-driven phase-out of oil and gas is both costly and unnecessary, as there is an alternative policy approach available that could achieve the same GHG reductions at a much lower economic cost to the country. This is the sense in which Canada would incur an “excessive cost” by phasing out its oil and gas production. The PPF/Navius report offers a credible and stark warning to anyone considering such a policy approach.

1. This “intermediate” scenario refers to the modelling scenario in which DAC technology is unavailable and most of the key variables discussed above—such as the world oil price and CCS technology—take on their intermediate values. It may or may not be the most likely of all the scenarios, but it is arguably the most “moderate”.

2. Another manifestation of the decline in Canadian national income in the case of the production phase-out would be a real depreciation of the Canadian dollar. As the production of oil and gas declines, Canada’s exports of these goods would also decline. The reduction in foreign purchases of Canadian exports would lead to a currency depreciation, which would reduce our purchasing power in global markets.

3. The growth rates in Table 2 are averages over the 30-year period, but there are important differences before and after 2035, the year when the production phase-out begins. With the production phase-out approach, Alberta’s GDP shows little growth between 2035 and 2050.

4. Readers may be wondering about the economic costs to provinces other than Alberta under the two policy approaches. The production phase-out approach is much more costly for Alberta but less costly for Ontario and Quebec because the nation-wide carbon price is lower under that approach. However, when summed across all provinces, the GDP cost is highest in the production phase-out approach, as is shown in Table 1.